Featured

Table of Contents

Pros: Teaches the thinking behind budgeting choices, not just how to execute them Centers on habits and habit development rather than faster ways or financial products Functions finest for workers who are already motivated to actively manage their moneyOffers a library of totally free workshops and education content included with the subscription Cons: The platform demands consistent, hands-on engagement something that can be a genuine barrier for staff members who are already overwhelmed by monetary stressEffective for capital management, but leaves gaps in locations like financial obligation technique, credit building, advantages optimization, and wider financial planningCoaching is available but comes at an extra cost to the staff member, rather than being covered as part of the employer-sponsored benefitPricing structure can be a stretch for smaller sized companies, particularly offered YNAB's narrow budgeting focus SmartDollar is a well-known name in the monetary wellness area, built on the Dave Ramsey brand name and a structured, step-by-step curriculum.

Pros: Strong brand name acknowledgment through the Dave Ramsey association provides the program immediate reliability with some employee populationsA clear, structured curriculum with defined actions and milestones makes development easy to trackA solid choice for organizations focused specifically on financial obligation reduction and structure foundational money habitsWills and trusts readily available through the platformSmartDollar coaches are trained exclusively on Ramsey principles and are not needed to hold formal financial credentials.

There is no customized strategy, just a recommended pathUser feedback points to a steep knowing curve, particularly when workers attempt to connect their real monetary image to the program's structureHR leaders report frustration with limited automation, consisting of the absence of built-in suggestions and a manual employee sign-up procedure that adds unneeded administrative problem Not all financial wellness platforms are developed the very same way, and the best concerns can expose a lot about whether a service is genuinely constructed for your staff members or built around an organization design.

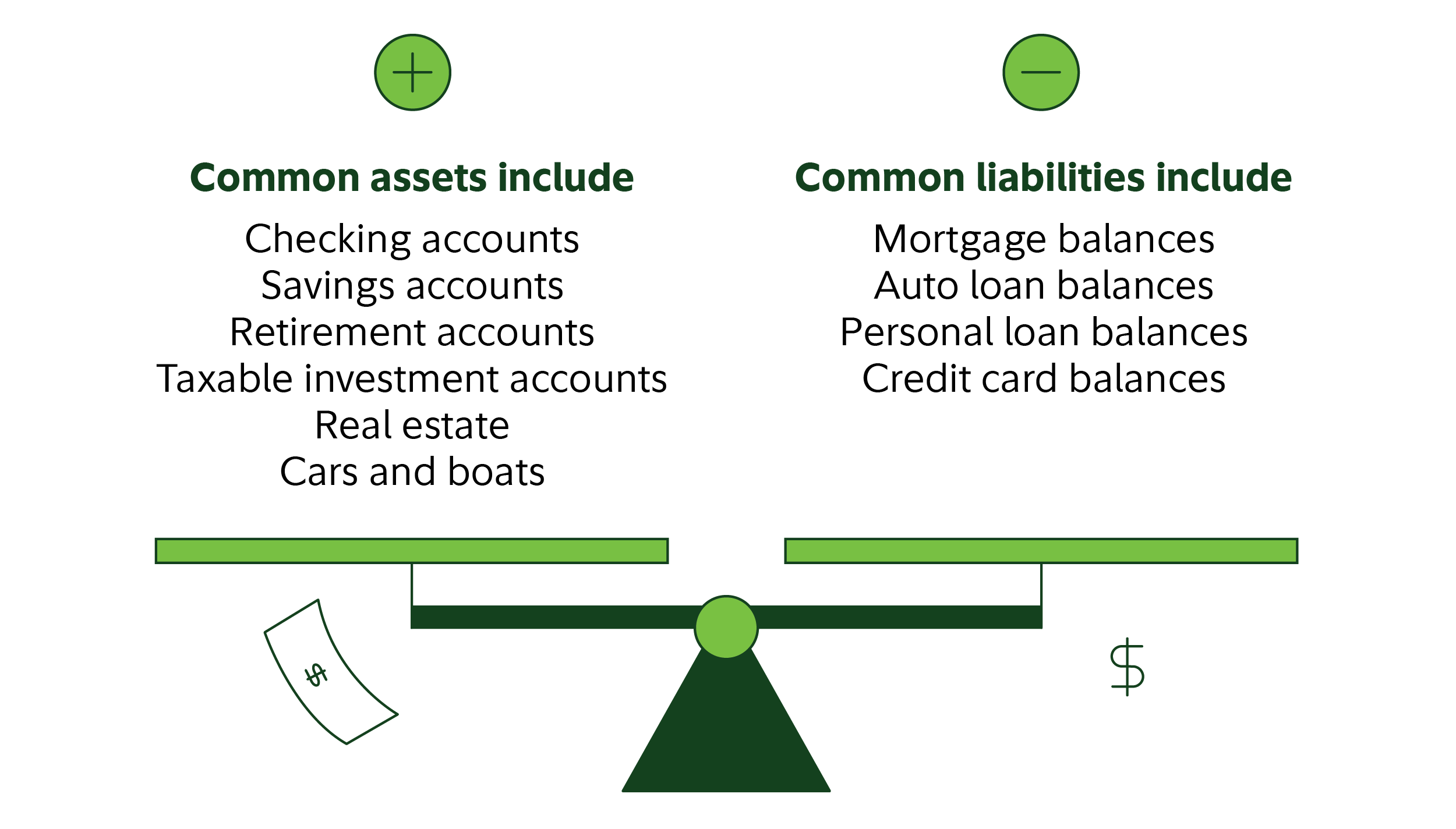

A service focused on loans and credit gain access to can provide short-term relief, however it doesn't attend to the origin of monetary tension. Your employees require a relied on resource that assists them budget better, develop credit, plan for the future, and make positive cash choices, without anyone benefiting from their battles along the way.

Simple Strategies to Save More Money During 2026Effective Ways to Save Capital in 2026

With endless access to licensed monetary coaches, AI-powered tools that personalize the experience at scale, and a model that never ever benefits from staff member financial obligation, YML delivers enduring modification, not just short-term relief. If you're all set to see what that looks like for your labor force, schedule a demo today..

What Makes an Excellent Personal Finance App in 2026?

2026 Financial Physical Fitness Passport. All rights reserved. For academic functions just. Not individualized monetary, legal, or tax suggestions.

Money-saving apps work by making your spending habits noticeable, which is the single most reliable step towards building cost savings. According to the Consumer Financial Defense Bureau (CFPB), individuals who actively track their finances are considerably more likely to reserve cash every month than those who rely on mental estimates alone.

Many people overstate just how much they save and undervalue how much they invest in small repeating purchases. A day-to-day $6 coffee routine amounts to over $2,100 per year. Membership services you forgot can drain $50 to $100 per month without you noticing. Cost savings apps expose these hidden costs by classifying every transaction.

How to Minimize Household Costs Next Year

You set spending limits per category and the app tracks your development, informing you before you review budget. You specify savings targets (emergency situation fund, holiday, deposit) and track progress with visual signs. Some apps rate your general monetary wellness, providing you a clear metric to improve over time.

The core principle is simple: what gets determined gets handled. A great cost savings app must include at minimum three core abilities: costs tracking with categories, savings goal management with development visualization, and spending plan production with notifies when you approach your limits. Beyond these essentials, look for a monetary health score, calculators for debt reward preparation, and privacy controls that keep your data secure.

Here is a priority-ranked breakdown of what to look for, starting with the functions that have the most direct influence on your savings: Whether you get in deals manually, import bank statements, or link via Plaid, the app requires to record every dollar in and out. Accuracy here is the foundation for everything else.

Guide to Federal Housing Counseling

Color-coded signs (green, yellow, red) make it simple to see where you stand at a glimpse. Development bars and portion signs offer motivation.

A 0-100 rating that examines your cost savings rate, debt-to-income ratio, emergency situation fund coverage, and expense-to-income ratio. This offers you a single number to track enhancement with time. Tools for loan benefit, charge card benefit, substance interest forecasts, and financial obligation snowball versus avalanche comparisons help you prepare before you act. Automated analysis that spots uncommon spending patterns, predicts future expenditures, and recommends budget plan modifications.

Payday-to-payday planning that shows how much discretionary cash you have after all obligations, not simply a month-to-month total. Income statements, money circulation reports, and export to Excel or PDF for tax preparation or sharing with a financial consultant. One feature that typically gets overlooked is where the app stores your data.

, which covers how to lessen costs consisting of subscription fees for monetary tools. The finest apps to save money in 2026 range from complimentary local-first tools to exceptional cloud-based platforms, each with different strengths in goal tracking, automation, and privacy.

Steps to Federal Housing Counseling

Here is how the top options compare side by side: App Expense Bank Connection Data Storage Budgeting Techniques Saving Features $0 $39/yr Handbook/ CSV/Excel/OFX/ QFX/PDF Any (zero-based, envelope, 50/30/20, pay-yourself-first, Runway, hybrid) Goals, budgets, health rating, calculators YNAB $109/yr (annual) or $14.99/ mo ($180/yr) Plaid (Cloud) Cloud Zero-based just Objective tracking, age of money Emperor Money $99.99/ yr (yearly) or $14.99/ mo ($180/yr) Plaid/ Finicity Cloud Passive tracking + objectives Goals, net worth tracking EveryDollar Free/ $79.99/ yr (annual) or $17.99/ mo ($216/yr) Plaid Cloud Zero-based just Financial obligation benefit tools Quicken Simplifi $71.88/ year Plaid Cloud Passive tracking + goals Spending watchlists GoodBudget Free/ $80/yr or $8/mo ($96/yr) Handbook Cloud Envelope just Envelope budgeting SenticMoney is a privacy-first budgeting application that shops all financial information on your gadget, not in the cloud.

{kind=link}

Latest Posts

Will Smart Financial Habits Improve Your 2026?

How to Boost Your FICO Score Fast

Why Debt Consolidation Helps in 2026